Aridor, Guy,

Duarte Gonçalves, Daniel Kluver, Ruoyan Kong,

and Joseph Konstan. 2022. The Economics of

Recommender Systems: Evidence from a Field

Experiment on MovieLens. ACM Transactions on

Economics and Computation (EC2023).

Ruixuan Sun,

Ruoyan Kong, Qiao Jin, and Joseph A. Konstan.

Less Can Be More: Exploring Population Rating

Dispositions with Partitioned Models in

Recommender Systems. 2nd Workshop on Group

Modeling, Adaptation and Personalization (GMAP

2023) .

Ruoyan Kong, Joseph A. Konstan.

The Challenge of Organizational Bulk Email

Systems: Models and Empirical Studies. The Elgar

companion to information economics. 2023.

Springer Publishing.

09/2018 -- (Ongoing),

Grouplens Lab, University of Minnesota,

supervised by Prof. Joseph Konstan.

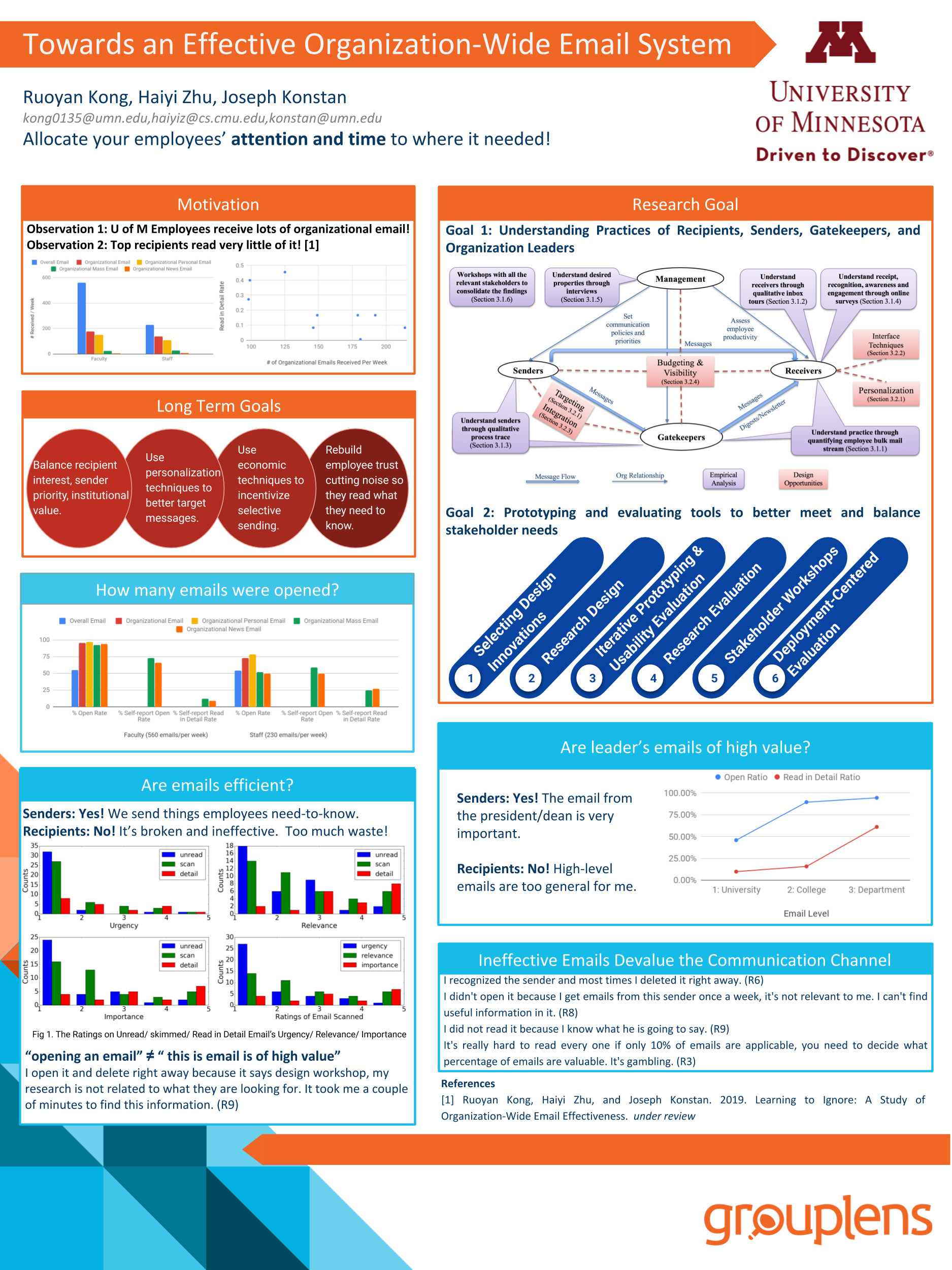

1. Towards an

Effective Organization -Wide Email System

1)In

organizations, Ineffective communication or

email overload could result in substantial

wasted employee time and lack of awareness or

compliance.

2)We study the reading behavior of employees

and interviewed representative organizational

senders to understand current practice, the

effectiveness of the communication channels,

and factors that lead to ineffective email

communication.

3)We found significant disorder and

ineffectiveness resulting in low read rates

and wasted employee time. A major factor

underlying these results is the disparate

views of different stakeholders on the use of

email channels.

4) I built a bulk email

personalization/delivering system which runs

for 2 months in a field experiment (python +

javascript + html), and a bulk email testing

platform which enables senders to evaluate the

time / money cost of each piece of information

within bulk emails (vue + html + firebase)

(https://bulk-comm.com/).

Ruoyan Kong, Chuankai Zhang,

Ruixuan Sun, Joseph A. Konstan.

Multi-stakeholder Personalization: A Field

Experiment on Incentivizing Employees Reading

Important Organizational Bulk Messages. To be

appeared in CSCW22.

Ruoyan Kong, Joseph A. Konstan.

The Challenge of Organizational Bulk Email

Systems: Models and Empirical Studies. The

Elgar companion to information economics

(under review). 2022.

09/2020 -

12/2020 Virtual Reality System for Invasive

Therapy

In invasive therapies such as

invasive ventilation and deep brain stimulation,

doctors face the challenge of planning,

performing, and learning complex surgical

procedures. VR systems were built to help doctors

plan surgeries. However, the previous VR designs

focused on navigation and visualization but not

risk estimation. In this paper, we introduced a

novel VR system for invasive treatment. Our

approach supports 1) 3D navigation of anatomical

models by a bi-manual miniature-world design; 2)

simulation of probe trajectory and calculation of

the corresponding risks; 3) visualization of

different layers; 4) visualization of

cross-sectional cutting by a plane. These

functions allow doctors to easily manipulate the

anatomical model and plan probe trajectory based

on the estimation of risks. https://www-users.cselabs.umn.edu/~kong0135/deepbrainvr/

09/2014-05/2016,

Department of Data Mining, National

Engineering Laboratory for Speech and

Language Information Processing,

supervised by Prof. Qi Liu.

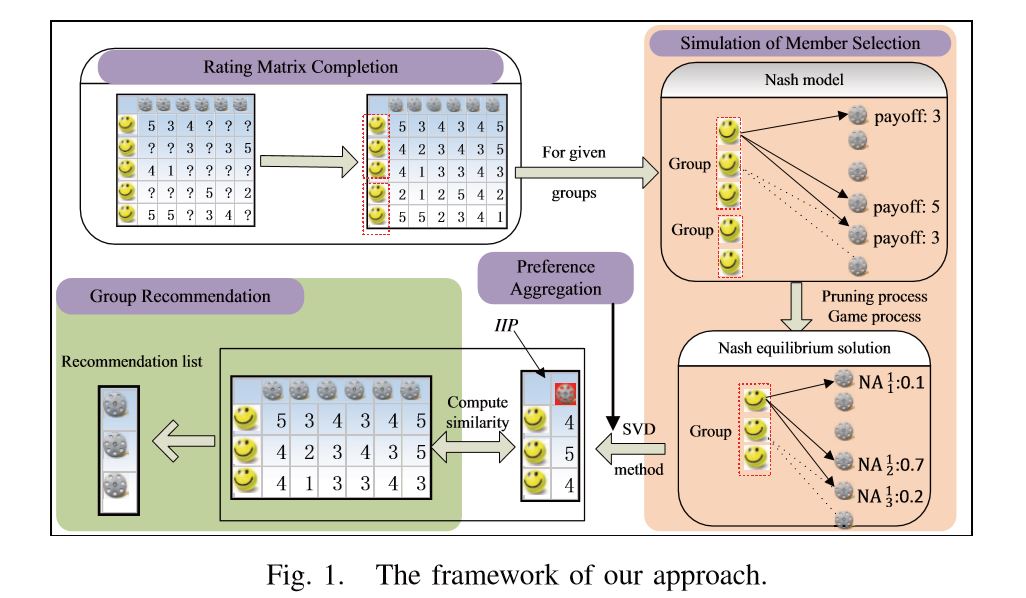

1. Design recommendation systems for group

users.

1)Group-oriented services such

as group recommendations aim to provide services

for a group of users. For these applications,

how to aggregate the preferences of different

group members is the toughest yet most important

problem.

2)In traditional preference

aggregation methods, such as preference

aggregation and score aggregation, the

interactions and fairness of group members are

still largely ignored. Therefore, these

aggregation approaches, which are unable to

figure out the optimal selections that can be

accepted by all members of a group, may lead to

unsatisfying services.

3) Inspired by game theory, we

propose to explore the idea of Nash equilibrium

to simulate the selections of members in a group

by a game process. The game process could

capture the group members’ interactions and the

Nash equilibrium solution considers the fairness

as much as possible.

4) Along with this line, we

first calculate the preferences (group-dependent

optimal selections) of each individual member in

a given group scene, i.e., an equilibrium

solution of this group, with the help of two

pruning approaches. Then, to get the aggregated

unitary preference of each group from all group

members, we design a matrix factorization-based

method which aggregates the preferences in

latent space and estimates the final group

preference in rating space. After obtaining the

group preference, group-oriented services (e.g.,

group recommendation) can be directly provided.

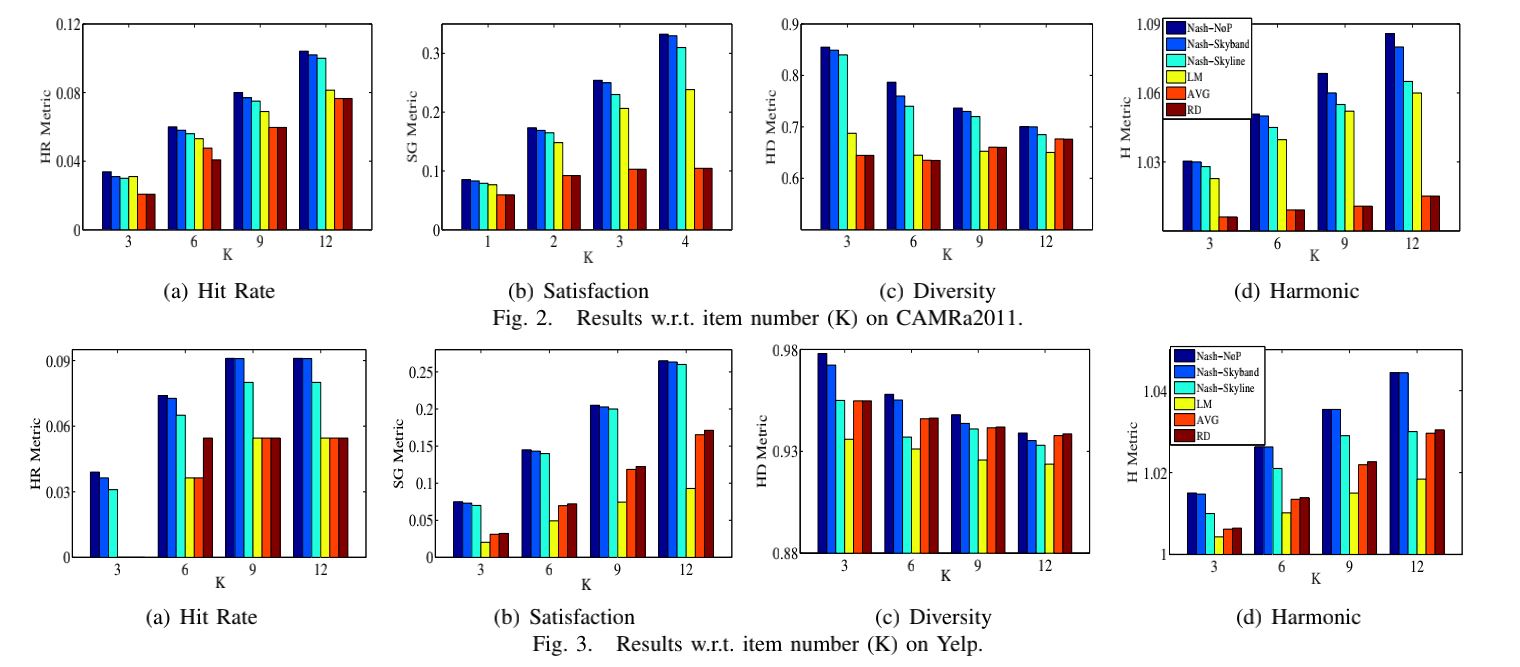

5) We examine our method on Yelp

dataset who has 22333 ratings. The results show

that the nash method has an outstanding

performance on 4 major metrics over other

methods.

6) Outstanding Student

Research, USTC, top 3% out of

undergraduates in USTC

Hongke Zhao, Qi Liu, Yong

Ge, Ruoyan Kong, Enhong Chen, Group

Preference Aggregation: A Nash Equilibrium

Approach, In Proceedings of the 16th

IEEE International Conference on Data Mining

(ICDM'16), Barcelona, Spain, 2016, 679-688

2.

Model of Incentives in Repeated

CrowdsourcingSystem

1) Repeated crowdsourcing

system refers to the crowdsourcing systems with

tasks which need to be conducted several times.

A problem needs to be solved in repeated

crowdsourcing system is how to set appropriate

incentives for requesters to maximize the

profits of requesters and workers.

2)Modeled the effects of

performance-contingent financial rewards in

crowdsourcing systems and provided answers to

the question: how does the anchoring effect

influence the cumulative profits of requesters and

workers?

3)– Proved that when the anchoring effect

coefficient r of requesters is smaller than 1,

the cumulative profits of requesters will

converge to a certain value increasingly, and

the value is negatively correlated with r. Tthe

optimal strategy for requesters is to increase

the wage slowly.

– Proved that when the

anchoring effect coefficient P of requesters is

smaller than 1 and r is smaller than P, the

cumulative profits of workers will converge to a

certain value increasingly, and the value is

negatively correlated with P.The optimal

strategy for workers is to increase the effort

slowly but keep it being larger than the

reaction of requester. Otherwise, the workers

should leave the game.

4) The crowdsourcing platforms

can use this model to design a principal scheme

to incentivize the participation of both

requesters and workers.

5) A-level undergraduate

thesis, top 10% out of undergraduates in USTC.

12/2016-08/2017

Department of Investment Management,

Derivatives-China, supervised by Mr.

You Zhang and Dr. Ling Long.

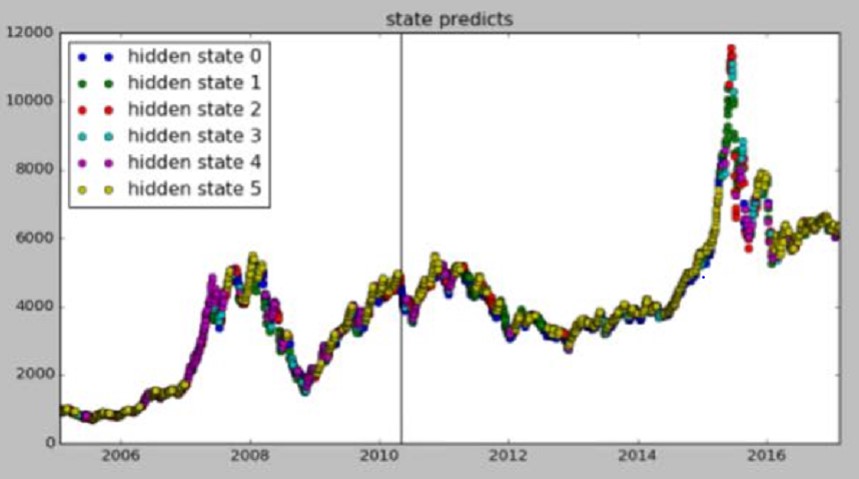

1. A Half-supervised Hidden Markov

Model to Forecast Index Futures.

1) In order to predict the

trend of markets precisely to make profits, we

use the hidden Markov model (HMM) to divide the

market into N different status.

2) The Baum-Welch algorithm

that is currently used to estimate the HMM only

converges to the local solution of HMM and can't

be applied in the real trading because its

result will change every time we optimize it. We

design a parallel-serial estimation algorithm to

solve this problem and got an approximate stable

solution. This is a creative work which has not

been done before.

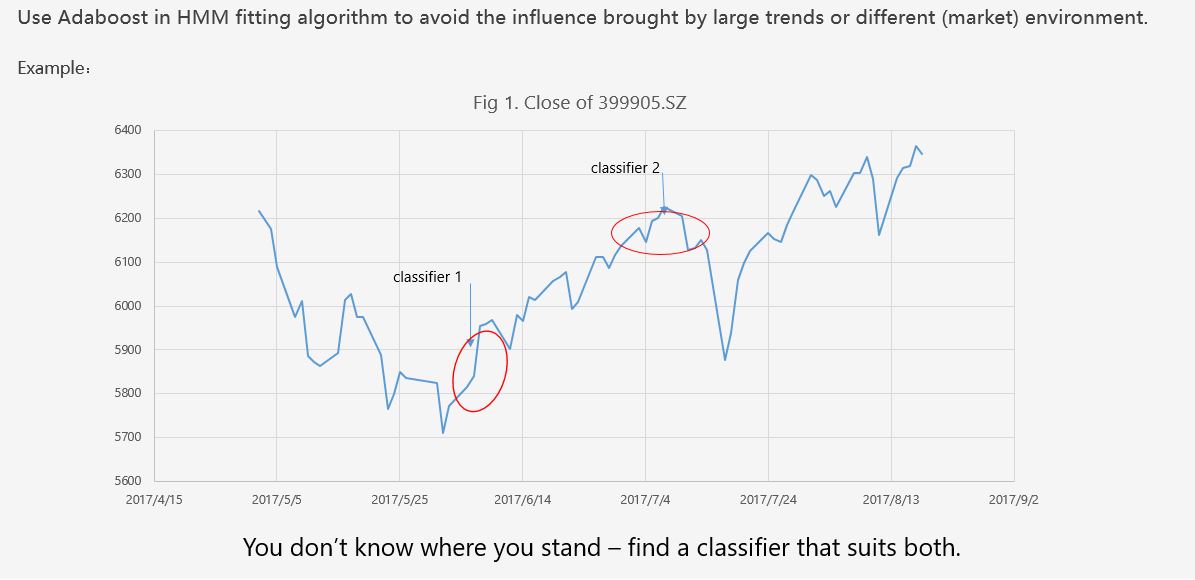

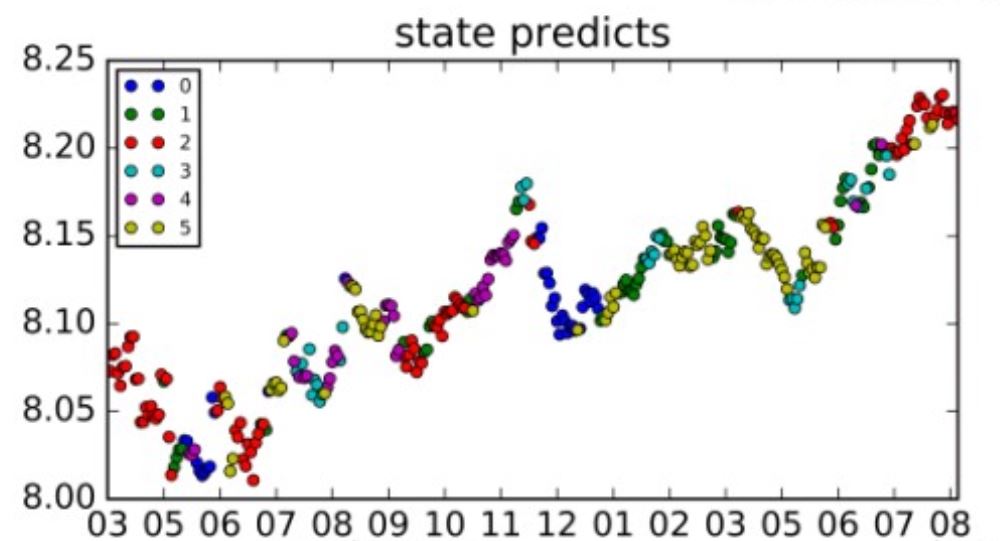

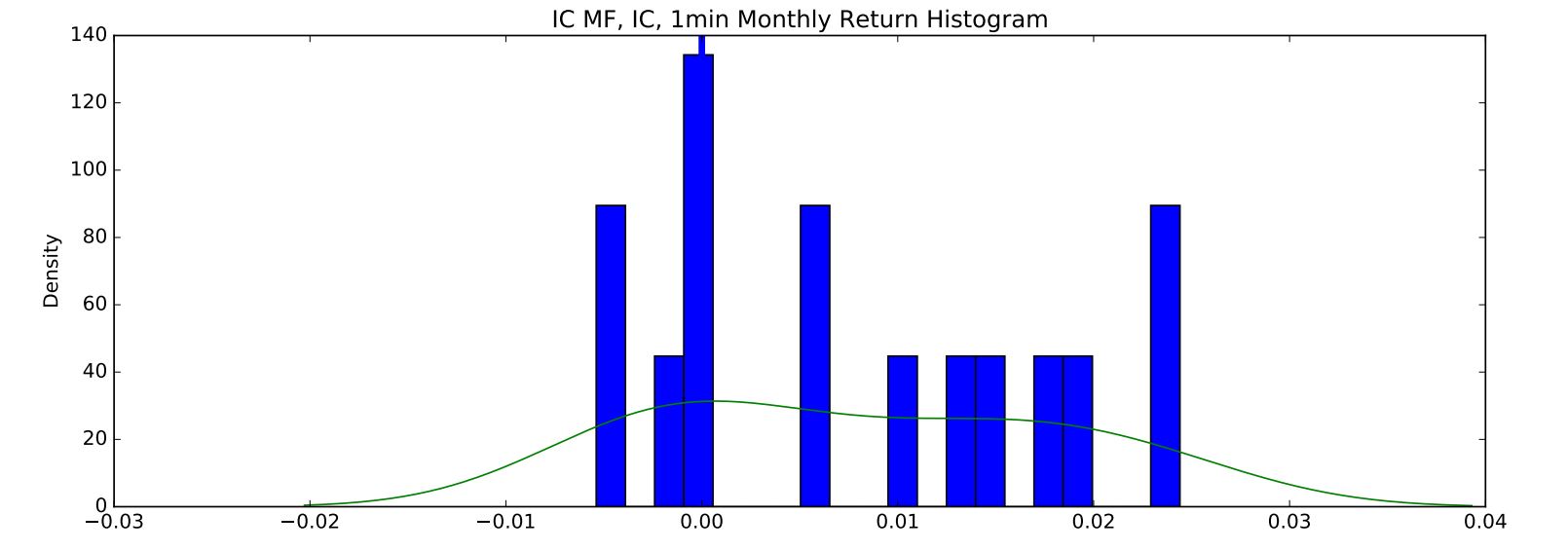

Fig 1.

The status of 399905.SZ predicted by HMM

(which gives a green warning before

the great market crash in 2015)

We can

find out that HMM has a good performance in

describing the market.

3) The

estimation of HMM is unsupervised and may not

towards the direction which we need to make

profits from. Also, the estimation process is

largely influenced by the big trend of the

economy, for example, the big trend of the

market from 2006 to 2015 is increasing, then

HMM will tend to give an increasing status

instead of taking the local situation of the

market into consideration. We need to build a

market timing strategy which can be applied to

different market environments.

Because

Baum-Welch algorithm and HMM include dependent

time series, we can't solve this problem by

simply enlarge the weights of negative

samples.

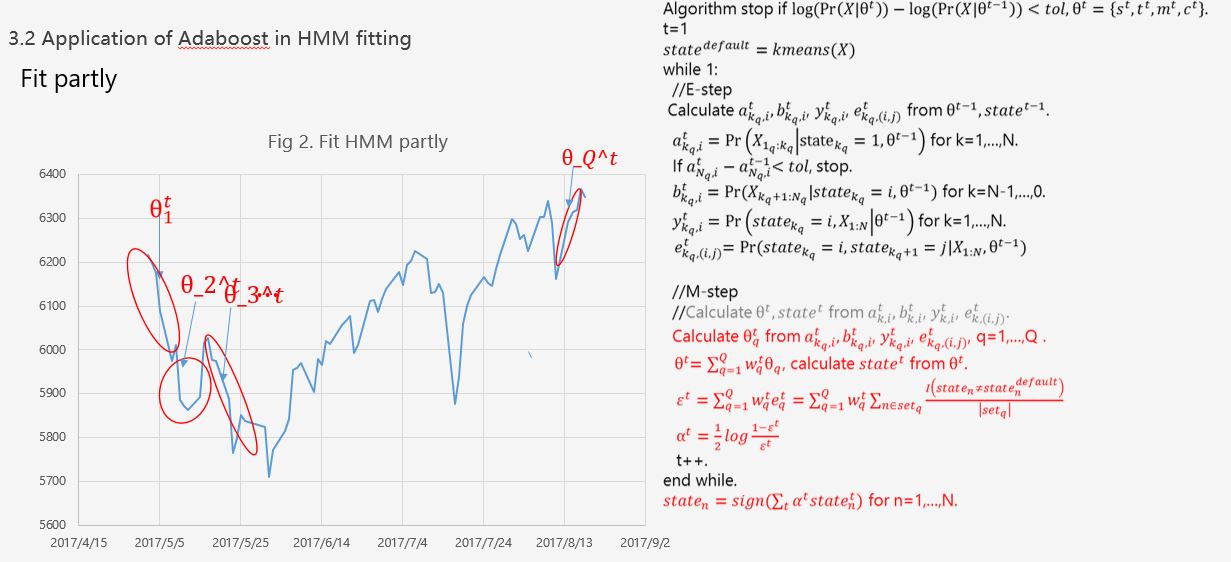

We use an

AdaBoost-subsection estimation method to solve

this problem. To our knowledge, this work has

not been done before.

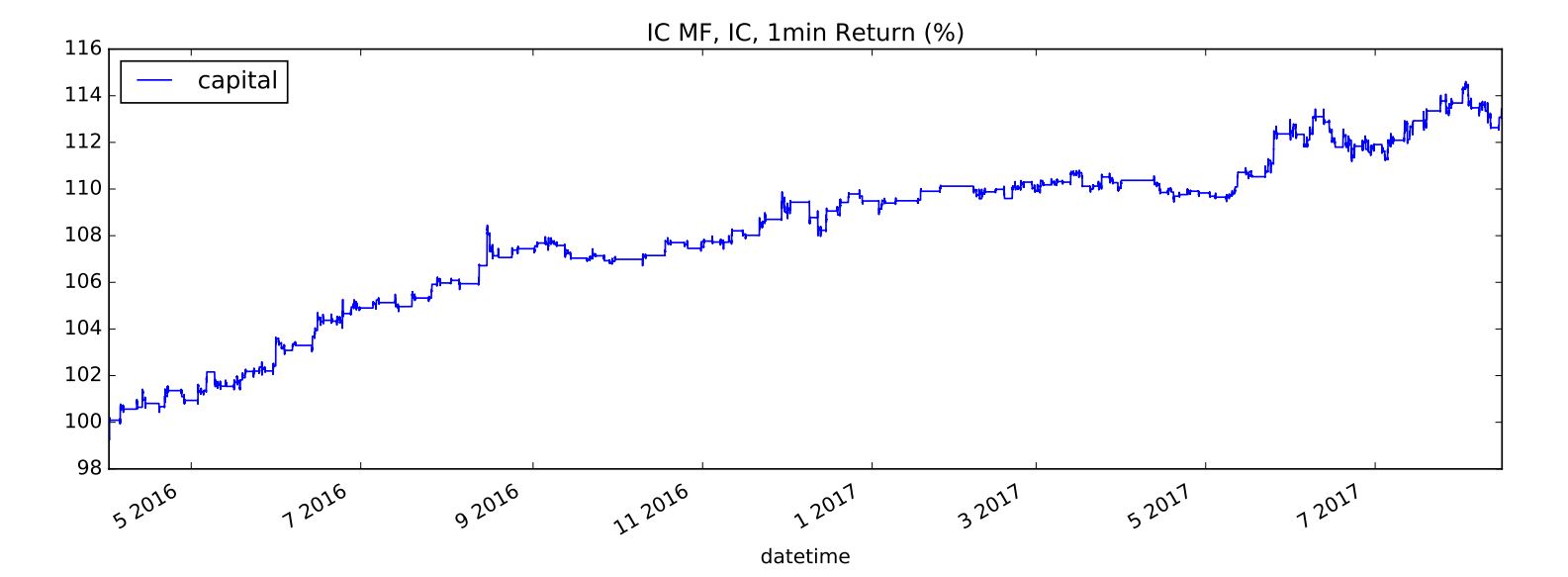

Our

algorithm has an outstanding performance in

predicting the trend of the market.

It can also bring a

consistent return.

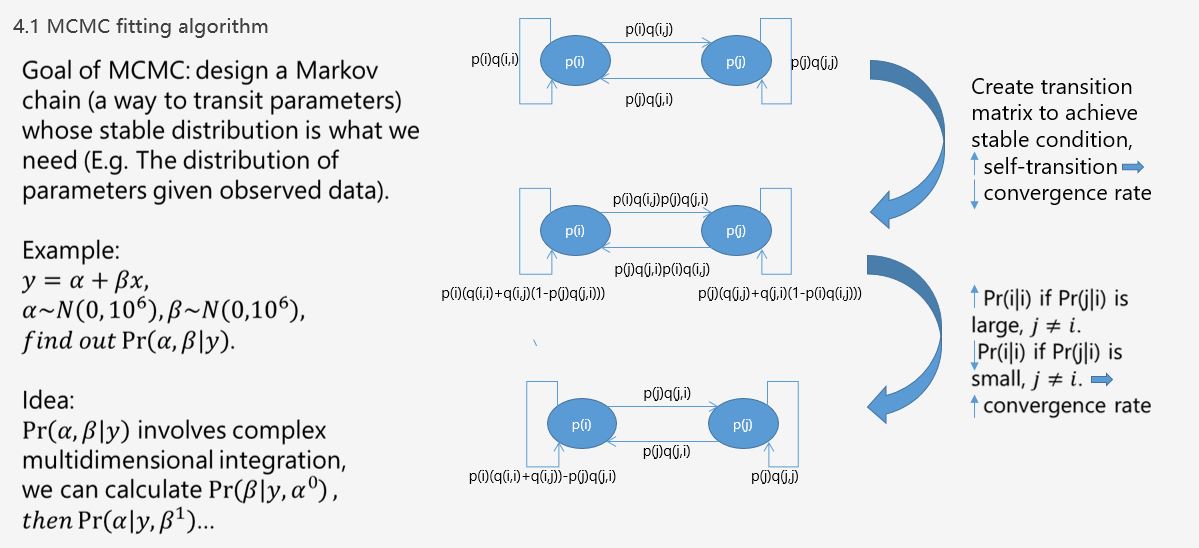

2. Application of Markov

Chain Monte Carlo (MCMC) and HMM in GDP

prediction.

1) If we want to apply

HMM in GDP prediction, we will find out that

the large scaling of features (E.g. the

overall GDP of last year) will keep us from a

good estimation of HMM, especially the means

matrix and covariance matrix in HMM. We need

to find a method to avoid this drawback of HMM

estimation algorithm.

2) We use Markov Chain

Monte Carlo (MCMC), which we can input our

prior information about the distribution of

parameters in, and Sobel Sequence can generate

highly independent random sequences. MCMC has

a Markov process which will converge to the

best estimation based on the posterior

distribution and the prior distribution of

parameters.

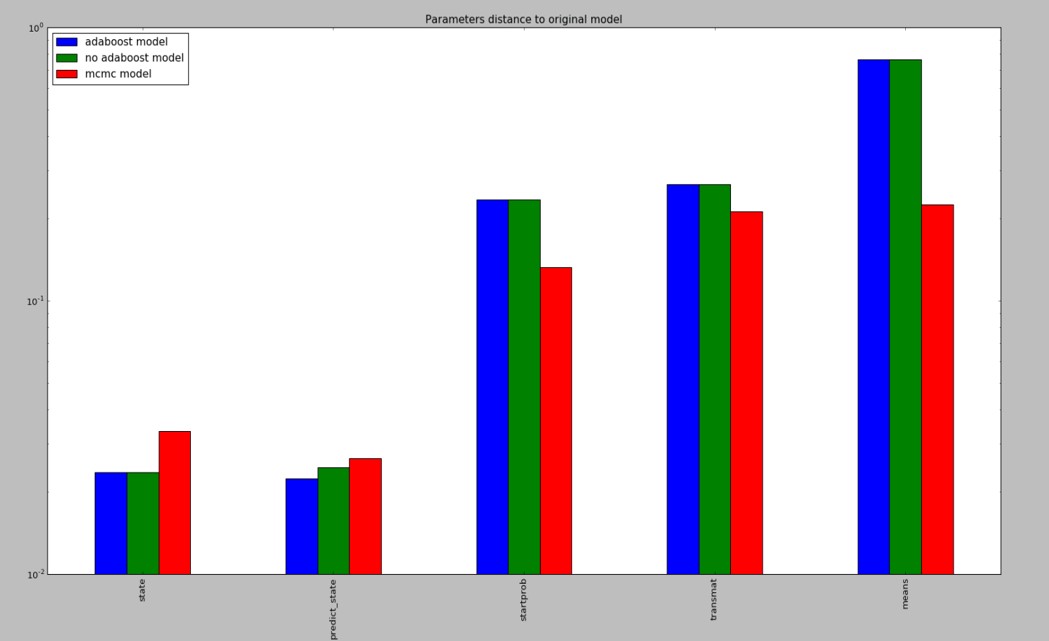

3) We can

see that MCMC has a lower error rate in the

estimation of parameters who have high

dimensions and large scalings.

Thanks to the beneficial suggestions from

Prof. Thomas J. Sargent.

09/2017-

06/2018 School of Economics and Management,

Tsinghua University, supervised by Prof.

Michael R. Powers.

1.A Risk

Finance Strategy Paradigm with Copulas

1) When dealing with risks, companies can

choose to pool, hedge or avoid them. However,

the traditional risk finance paradigm can't give

a quantitative method to describe the condition

of the application of these strategies.

2) In our prior work (Risk Finance for

Catastrophe Losses with Pareto-Calibrated

Levy-Stable Severities, Michael R. Powers), we

used stable distributions to model this

paradigm. In this paradigm, we assume that

losses are independent, which is consistent with

our real experience.

If we assume losses are correlated, the

paradigm would be different. The reason for

taking correlation into consideration is that

correlation between losses will affect people’s

decisions about whether to hedge or pool the

loss portfolio L. For example, a group of marine

traders wants to limit their ship sinking risks.

If their routes are different, their ship

sinking risks are uncorrelated and they can

divide their merchandise into portions and

distribute across all ships (pooling), then no

trader will be devastated by a sinking of one

ship. However if their routes are the same,

their ship sinking risks are correlated (their

ships may be attacked by hurricanes or tidal

waves together), then pooling will be useless in

this case because they will be devastated by the

sinking of ships altogether and they should

choose to hedge this portfolio like to buy

insurance from an insurer (who can afford this

because he can pool the risks from different

marine trader groups).

3) We also designed a parallel-serial numerical

algorithm to get Fourier-analytic risks for

levy-stable variables.

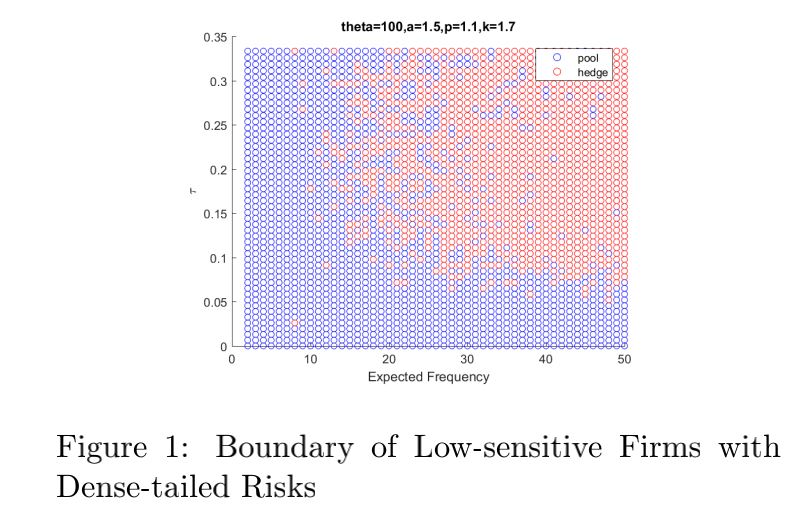

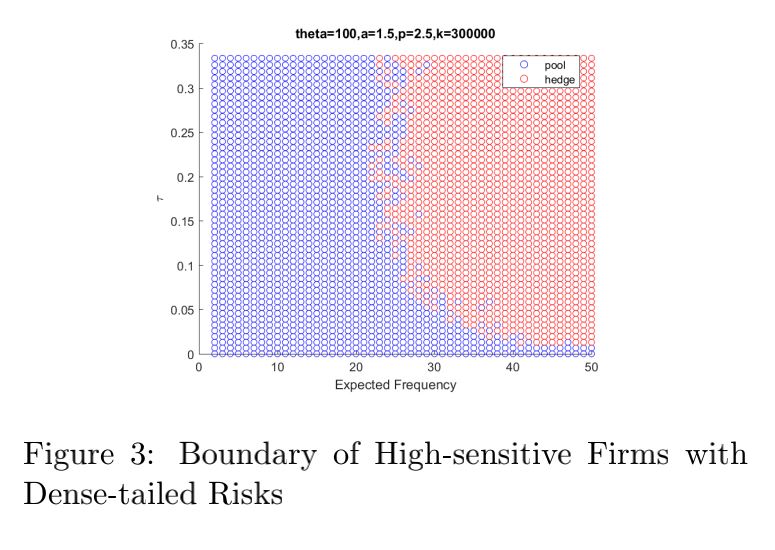

4) Heavy-tailed case: As p increases, the firm

will be more sensitive to risks, and the lower

boundary will decreases more rapidly as the

expected frequency increases. It can be observed

that when p < 2, a firm will still choose to

pool when the dependence between risks is as

small as the expected frequency increases.

However, when p > 2, as the expected

frequency is large enough, the firm will always

choose to hedge no matter the dependence is

small or not.

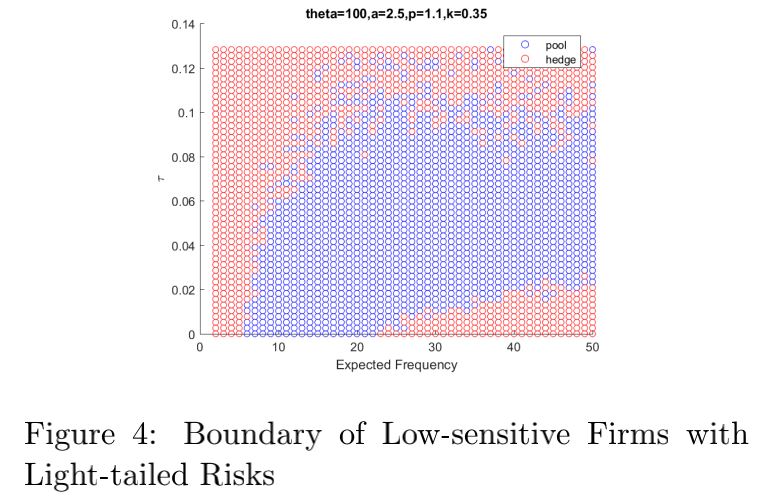

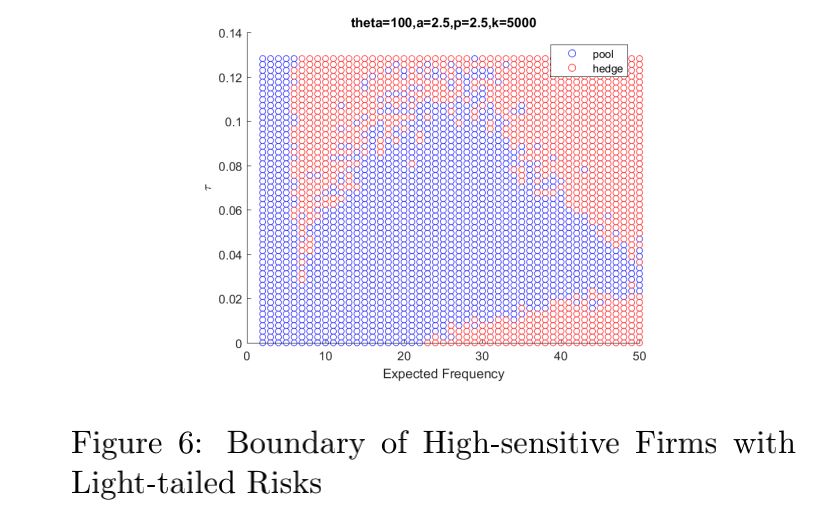

5) Light-tailed case:

When the expected frequency become a little

larger, the firm will be able to accept higher

dependence(TypeII). It may be attributed to that

a little larger frequency offers more choice for

the firm to distribute the risks.

When the expected frequency achieves some

point, the firm can only accept lower dependence

as the expected frequency increases(TypeI). It

may be attributed to that higher frequency will

increase a firms’ overall risks to a large

extent. And an interesting inverse lower part

appears(TypeIII). In this part, the firm will be

exposed to high frequency and low dependence

risks, and it will choose to hedge to diminish

the risks brought by the high frequency.

As p increases, the firm will be more sensitive

to risks, and the lower part of the TypeI

boundary will decreases more rapidly as the

expected frequency increases. When p > 4/3,

the hedging districts in the right-upper corner

and in the right-lower corner will merge when

the expected frequency is large enough, which

means that the firm will always choose to hedge

when the expected frequency is large enough.

When p < 4/3, there will always be a room

left for pooling no matter how larger the

expected frequency will be.